Freight Market Update for Q1 2026

Welcome to our first Market Watch of 2026. After a year defined by hesitation, we are providing a concise look at the forces that shaped 2025 and setting expectations for the year ahead. As we exit a period of freight rate stagnation, the market is shifting. We are now looking at an environment where supply constraints are creating a familiar reality for shippers and carriers.

A Note from Chris Pickett, Our Chief Commercial Officer

We are entering a time where there is arguably more demand than supply, signaling that we are firmly in an inflationary leg of the freight cycle. To understand where we are going, we must look at the factors that brought us here. The 2025 freight market was defined by a tug-of-war between demand-side hesitation and supply-side corrections. On the demand side, U.S. trade wars and tariff uncertainty dampened market recovery, causing procurement teams to hold orders in limbo. On the supply side, a crackdown on CDLs and fluctuating diesel prices accelerated the exit of non-compliant capacity, slowly tightening the floor.

Holiday data points to a cyclical shift, not just seasonal. December DAT linehaul van rates surged 15% month-over-month, compared to a +5% lift in 2024 & 2023, and +3% in 2022. We believe the recent relative surge in spot rates has been driven more by capacity exiting the market than by a massive increase in demand. As regulatory scrutiny accelerates the departure of carriers who were artificially suppressing rates, the remaining fleet is compliant and pricier. The floor has been raised, and the market is responding accordingly.

The Freight Market Trends You Need to Watch

As we navigate this new cycle, keep a close eye on these critical factors shaping capacity and cost:

- Tightening trucking regulations: Watch for continued government crackdowns on CDL compliance. This regulatory scrutiny is actively reducing the pool of available drivers, accelerating the exit of non-compliant capacity that previously kept rates artificially low.

- Diesel price volatility: While diesel prices have been sliding lower over the past two months (down ~9%) and are currently ~5% cheaper on a year-over-year basis, we’re keeping an eye on it. Any upturns in fuel costs will put immediate upwards pressure on an already rising floor for truckload prices.

- Demand catalysts: We are in an inflationary cycle regardless of demand, but specific catalysts could exacerbate conditions. Demand-side activity remains the biggest wild card for 2026. Monitor factors like inventory restocking, a thawing housing market, manufacturing recovery, or any resolution on tariffs that releases pent-up shipping volume.

Key Freight Market Insights for 2026

- Q1 Spot Rate Outlook: We predict Q1 spot rates will settle at +10% year-over-year, plus or minus 5%. While we expect some fading from the January highs, the floor remains elevated compared to 2025.

- End-of-Year Spot Rate Forecast: Without any major demand catalyst, spot rates are forecasted to reach a year-over-year increase of +25% to +30% by the end of the year based on supply attrition alone.

- Impact of Demand Catalysts: If we see significant movement in manufacturing or tariff resolution, demand catalysts could push end-of-year spot rates even higher, potentially reaching +30% to +40%.

- Contract Rate Trajectory: Contract rates will follow the spot market's lead, likely reaching +6% year-over-year by the end of 2026 as routing guides come under increasing pressure.

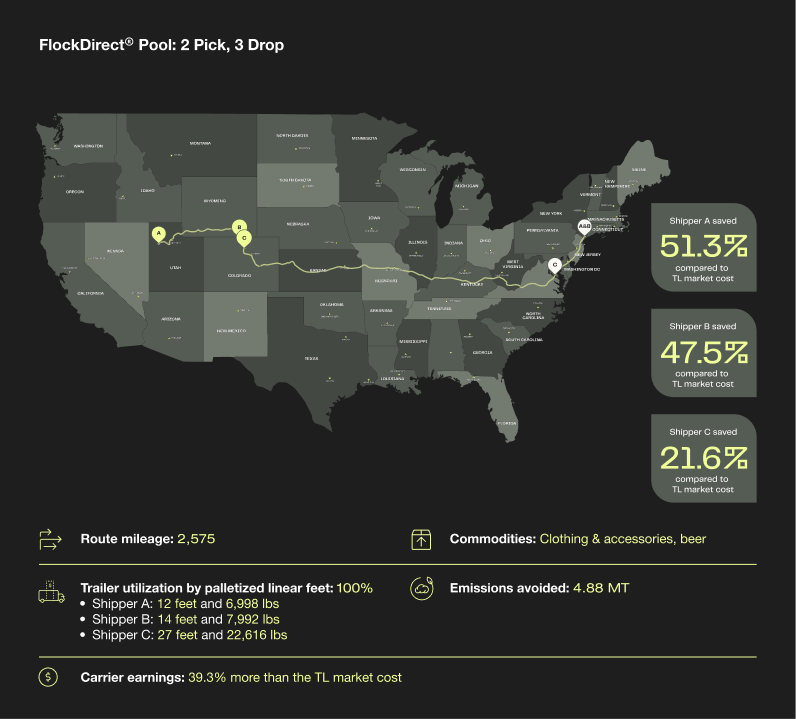

Shared Truckload Spotlight

Ever wonder what a FlockDirect® Shared Truckload looks like in practice or their real-world impact? Join us on a virtual road trip to see how our recent FlockDirect® shipments are redefining traditional shipping.

Looking Ahead

Shippers should consider which levers are available to mitigate volatility and position themselves to win. In the market we’re entering, carriers will be in a stronger position than in years prior and will naturally become pickier about the freight and rates they accept. Consequently, shippers will start feeling increased pressure from carriers to reprice contract rates earlier than expected.

To navigate this, shippers need to proactively explain budget variance to leadership and offset rate increases by shipping more efficiently. A quicker win that will benefit shippers even in a deflationary market, is to reduce their spend on half-empty truckloads. Flock Freight’s Shared Truckload (STL) service, FlockDirect® lowers costs by an average of 20% by sharing trailer space with compatible Flock shipments. Shippers are maximizing trailer space without changing load sizes, avoiding up to 40% of emissions, and protecting themselves against inflation by integrating STL into their 2026 strategies.

.jpg)