Freight Market Trends and Forecasts for Q3 2025

.jpg)

Despite a volatile economic backdrop marked by tariff uncertainties and geopolitical tensions, the U.S. economy has shown surprising resilience through Q2 2025. However, with freight market indicators beginning to wobble, the question remains: is this the calm before the storm? This blog dives into the key trends and insights shaping the freight market forecast as we navigate Q3 and beyond.

A Note from Chris Pickett, Our Chief Commercial Officer

Through Q2, despite increasingly volatile US trade policy and the specter of a new wave of tariff-driven consumer price inflation, the US economy has largely held. Is this the calm before the storm? Or does the resilience of the US consumer persist yet again?

We didn’t see any material rise in consumer inflation, nor degradation in consumer spending or industrial production in Q2, but indicators did start to wobble a bit compared to a surprisingly strong Q1. From a macro standpoint, the economy is doing well enough, such that a recession certainly does not appear imminent. And as it stands, the predicted post-April 2nd Liberation Day industry apocalypse hasn’t happened yet…and likely never will, considering the progress on bilateral trade deals with major trading partners and what continues to be a relatively tame inflation backdrop.

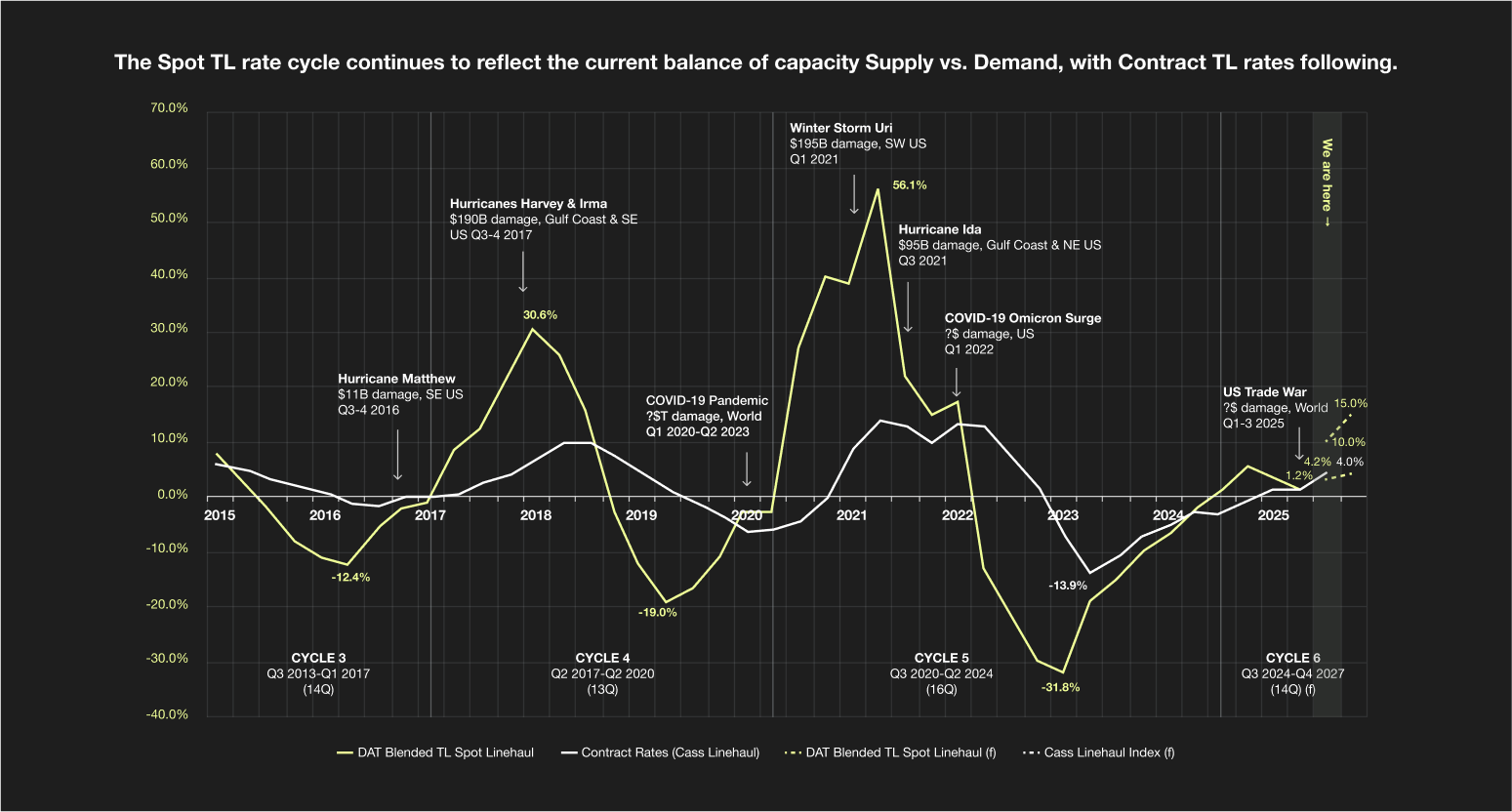

Coming into this year, based on the momentum coming out of Q4 2024, we expected the Y/Y inflationary leg in this new spot market truckload rate cycle to be off and running, reaching +5% Q2. Instead, we closed at +1.2%, and down materially from Q1’s +2.4% Y/Y. So after the longest deflationary leg of a cycle on record, we’re now stuck bouncing along equilibrium for the third consecutive quarter, which is a first and is believed to be the result mostly of tariff uncertainty for consumers and global supply chains alike.

The Freight Market Trends You Need to Watch

Durable & nondurable goods consumption

We’re back to pre-COVID consumption levels of durable and nondurable goods, while service consumption is mostly flat. But despite this relative strength in goods consumption, freight capacity demand has remained tepid at best in recent quarters, which has helped keep a lid on spot and contract truckload freight market rates.

Relative inventory levels

After trending lower in recent quarters, the Inventory to Sales ratio started to bend higher in Q2. This was expected, given the surge in import activity in Q1 2025 implying a pull forward in orders for many US importers from tariff-exposed countries like China. As we all know, rising relative inventory levels act as a headwind for US industrial activity and therefore the demand for truckload capacity.

Industrial production

IP was running flat YoY for the past 7 quarters and starting to trend upwards in Q1, closing at +1.5%, before weakening in Q2 to +.9% Y/Y. This was another somewhat bearish sign for US spot linehaul rates, at least in the near term.

Wild cards

- Tariff overhang keeping a lid on overall consumption and industrial activity, and preventing otherwise normalized demand patterns from affecting the macro economy and ultimately trucking conditions.

- Ongoing geopolitical tensions in the Middle East, Taiwan, and Ukraine.

- The direction of diesel prices. When diesel prices spike, that pushes supply out, all else equal. And with costs up 15 cents/gallon or +7% over the last two months, we could start to see carrier exits accelerate as a result.

Key Market Insights for Q2 2025

Q3 spot linehaul rates are now predicted to close at 5% + 5.0% Y/Y, with contract rates following closely behind at +3% + 2.0%, down materially from the forecast coming into the year and before the first shots of the US trade war were fired.

Based on supply exit alone, we believe there is still a case for an increasingly Y/Y inflationary freight market prediction in the US over the balance of the year. We don’t expect a shock given the tariff overhang that remains, but rather a gradual climb over the next two quarters and into 2026. As a result, barring a collapse in demand, Q4 could close with spot rates reaching +10%-15% Y/Y with contract rates reaching +4-6%.

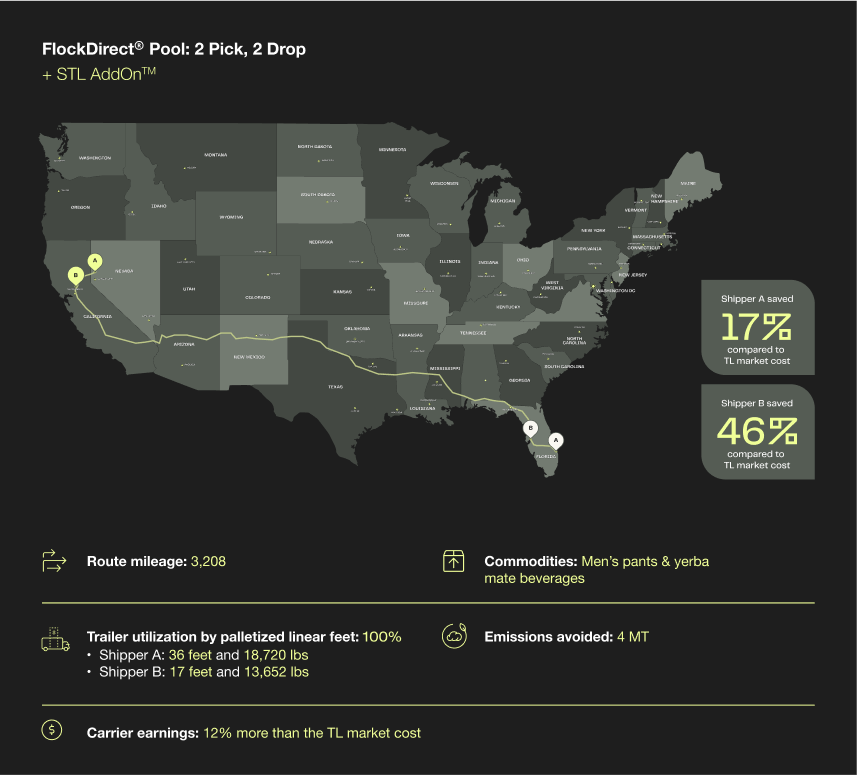

Shared Truckload Spotlight

Ever wonder what a FlockDirect® Shared Truckload looks like in practice or their real-world impact? Join us on a virtual road trip to see how our recent FlockDirect® shipments are redefining traditional shippiing.

Looking Ahead

Tariff back-and-forth hasn’t had as strong an effect on freight costs as the news cycle predicted. Truckload rates will likely rise in the last half of the year, but it will have less to do with tariff-driven commodity inflation and more to do with the natural cycle of the trucking industry. Still, there is a need for speed in this uncertain environment, where the market cycle of the last 20 years isn’t taking the turns we expect at the time we expect them. While shippers are secure and happy with their rates, build those carrier relationships and move any inventory you can. We don’t know what next quarter brings.