Understanding Freight Shipping Insurance: A Comprehensive Guide

An unfortunate reality of shipping freight is that, despite your best efforts, items will sometimes get damaged, lost, or even stolen in transit. As your business grows, your costs—including those you stand to lose in the event of a mishap—grow alongside it.

One way to mitigate your risk is to purchase freight insurance. These supplemental policies help protect your shipments beyond what your carrier liability stipulates.

What is freight insurance?

Freight insurance is a supplemental insurance policy that covers your cargo while it is in transit with your chosen shipping carrier. Much like homeowners insurance protects your valuables in the event of a disaster, freight insurance can protect your goods against damage, theft, or loss while on the road. Freight insurance can cover the cost of replacement or repairs of some or all of those goods, depending on the extent of your policy.

Carrier liability vs. freight insurance

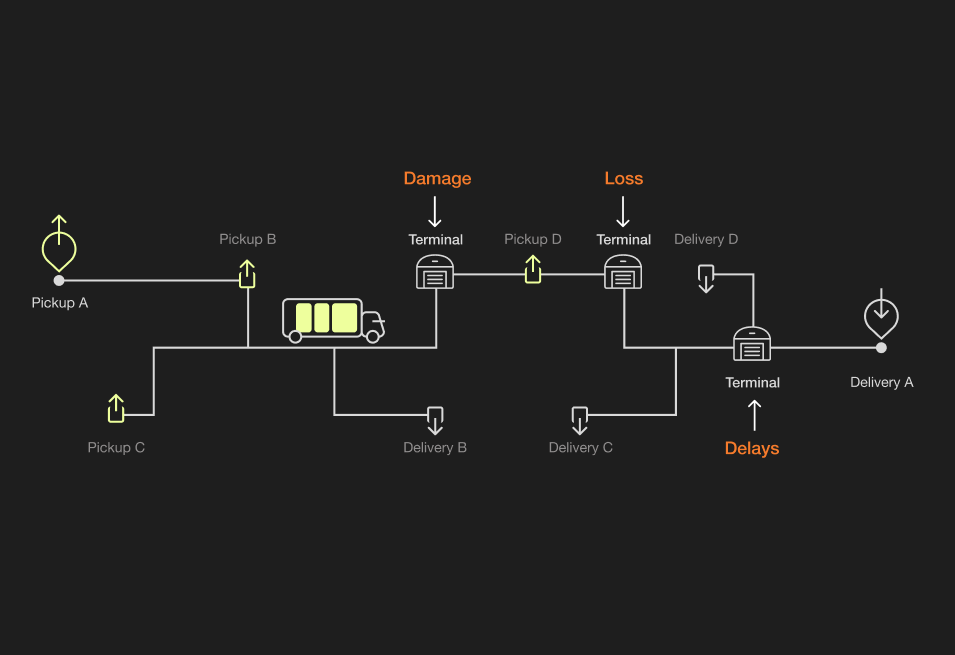

Once your goods leave your business or warehouse, the entrusted carrier assumes responsibility for the safety of those items. Carrier liability is what the shipping company is legally responsible for during transport and/or storage. Should any loss, theft, damage, or other specified issue arise, they will cover the cost of the affected goods up to their maximum liability. Carrier liability coverage is based on several factors, including the transportation mode, the freight class your goods fall into, and the type of commodities you’re shipping.

Freight insurance is a separate policy that bridges the gap between your carrier’s liability and your own responsibility. Should the value of the damaged or lost product exceed the carrier’s maximum liability, your freight insurance policy will kick in to cover the remaining cost.

What does freight insurance cover?

Freight insurance policies can cover any or all of the following risks:

- Loss

- Theft

- Physical damage, whether due to mishandling, accidents, or extreme weather

- Non-delivery of goods

- Infestation

- Government seizure

Not all freight insurance policies cover all of the above. For example, depending on your type of freight insurance, you may be protected against damage from natural disasters like hurricanes or tornadoes but not for delayed delivery due to weather-related events.

Common freight insurance exclusions

Certain scenarios may be excluded from your freight insurance coverage regardless of your policy. These include:

- Poor packaging of your goods

- Inaccurate labeling of your shipment

- Normal wear and tear incurred during the shipment process

- Shipment and delivery delays

There are also specific goods that may not be covered by freight insurance. Commonly excluded items include:

- Weapons and ammunition

- Alcohol

- Precious metals and gemstones

- Artwork and antiques

- Tobacco products

- Traded metals

- Electronics

- Pharmaceuticals

Make sure to verify what is covered—and NOT covered—in any insurance policy you’re considering. Depending on the scenario and/or shipped goods, you may still be able to specify some exclusions in your policy and get them covered. If you opted for a named perils policy, for example, you could ask to specify delays as a covered risk. Also note that some policies may require a claim to be valid against the carrier before they will pay out.

Types of freight insurance

There are several different freight insurance types to choose from. These policies differ in what perils or causes of damage or loss they cover; and what types of loss or damage they will pay out for; and what items are covered. Some of the most common cargo freight insurance policies include:

- Basic coverage: Offering the least amount of coverage, basic freight insurance covers only limited perils. The insurer only covers specific causes of damage to your goods, or they may exclude certain items from coverage entirely. For example, they may cover damage due to an accident or a natural disaster, but not that caused by careless handling.

- Named or specified perils coverage: This type of freight insurance policy protects against specific types of hazards, risks, or perils that are outlined within the policy. If a type of damage occurs that isn’t named in the policy, the insurer will not cover it. For example, a named policy could specify coverage of damage from a tornado or a hurricane but not from severe flooding. A specified perils policy is often designed around the type of cargo being transported.

- Broad coverage: This policy offers more protection than basic or named coverage but not as much as all-risk coverage. Broad freight insurance coverage will compensate for all damage or loss to your cargo but includes specific exceptions set forth in the policy. These are often personal items, such as personal electronics or money.

- All-risk coverage: The most comprehensive protection, all-risk cargo insurance covers any damage or loss due to any external cause. This could be an accident, a natural disaster, mishandling, theft, or even poor storage of your goods before, during, and after transit.

- Total loss-only coverage: As the name indicates, this type of freight insurance kicks in only when the entire shipment has been compromised rather than individual pieces or minor damage.

- Contingent coverage: A contingent cargo insurance policy is a supplementary safety net for any coverage gaps in your primary insurance policy. If, for example, your shipment’s total loss is more than your policy’s limits, or if your insurer denies a claim, your contingency insurance would cover the difference.

Note that some carriers and brokers offer additional insurance to purchase as an add-on to their policies. Before buying, make sure you understand what type of insurance they’re offering you and how it may impact your overall coverage—for example, you may think the additional policy, combined with the initial carrier liability, equals out to all-risk coverage, but may in fact only equal “excess” cargo coverage.

How much does freight insurance cost?

Your freight quote should include the carrier’s liability coverage, but any additional freight insurance is an add-on cost. On average, freight insurance costs between 1-2% of goods’ value. That said, the price of your freight insurance policy depends on several factors, including:

- Coverage level—the more protection you want, the more you’ll pay.

- Item value—the more expensive the goods, the more they cost to insure.

- Risk factor—the higher the likelihood of your goods being stolen or damaged, the higher your policy cost will be.

- Where you’re shipping to and from—the longer your goods are on the road, the higher the risk (and therefore the higher the cost).

- The carrier’s history—If your shipping company has a track record of being party to insurance claims, supplemental freight insurance will cost more.

As you’d imagine, all-risk coverage is the most expensive but also the most comprehensive. Opting for all-risk coverage ensures that no matter what happens, your goods are protected. On the flip side, basic or named perils coverage policies are more affordable but also provide only limited protection on specific items. You will be responsible for the remaining cost of goods should an incident occur outside of your policy’s stipulations.

Why freight insurance is vital for businesses

As a business owner, you need to be keenly aware of every penny going in and out of your P&L. Many companies make the mistake of relying on their carrier’s liability coverage, not realizing that it may not cover the entire value of your shipment. In fact, the type of goods you’re shipping can impact their value per pound—shipping used books versus brand-new electronics could significantly reduce the liability value.

Freight insurance bridges that gap and offers door-to-door protection depending on your chosen policy. Plus, you can customize your coverage to your business’ needs and budget. A named perils policy, for example, allows you to cover against the specific risks most important to you, thereby cutting costs by not covering those that don’t necessarily apply to your business.

How to choose the right freight insurance coverage

Check your carrier’s liability

Before determining what supplemental insurance you want, you must understand your carrier’s legal responsibility. Each carrier’s list of risks it will protect against varies, and you may find significant gaps in coverage with one carrier, while another offers most of the protections you’re looking for.

Assess the types of goods you’re shipping

First, take stock of what you’re placing on those trucks. Are your items high-value, perishable, or fragile, or are they less expensive and not easily broken? Are you shipping expensive, theft-prone laptops, or relatively cheap and durable plastic parts?

If your items are likely to break, rot, or get stolen—referred to as “inherent vice of the product”— you’ll want a more comprehensive policy to protect yourself against outsized replacement or repair costs. All-risk coverage is a better choice for items at higher risk of theft or damage or those that are of higher importance than other shipments. Make sure this is covered in your policy, either within the initial terms or added as a specified peril.

If your items are sturdy, non-perishable, and not extremely expensive or theft-prone, you can likely get away with a more affordable freight insurance option, like a basic or named perils policy.

Compare shipping carriers & insurers

Cargo insurance is not required by law, nor is it tracked or verified by the Department of Transportation (DOT). Therefore, it’s important to compare carriers, brokers, and insurance companies to find ones you trust to protect your goods (and your bottom line).

As mentioned above, your carrier’s history and reputation go a long way toward keeping your freight insurance cost low. If a carrier has a track record of losing or damaging cargo, you may want to look elsewhere—not only to keep your insurance overhead lower but also to better protect your goods from the outset.

Comparing carriers also allows you to find an option that meets your budget. Get quotes from several carriers and find one that offers breathing room within your bottom line. Similarly, any additional freight insurance outside the carrier liability will be an additional cost, so shop around for an affordable insurer with a good reputation for advocating for their shipping clients and paying out when needed—without hassle.

Ship easily and safely with Flock Freight

Flock Freight can help partner you with a reliable shipping carrier you can trust to deliver your goods safely. While 89% of shippers were negatively impacted by theft or fraud in 2023, Flock Freight delivered a 99.8% theft-free rate for all shipment types in the same year. Plus, by skipping hubs and terminals with Shared Truckload (STL), the risk of damage drops by 7.5x versus traditional less-than-truckload (LTL) shipping.

You can also choose from a variety of insurance offerings, with up to $100,000 in standard liability coverage for all carriers in the Flock network. Need additional protection? Choose Excess Insurance when getting your shipping quote—simply select “Yes” for additional insurance. Learn more about Flock Freight’s low-risk STL shipping and request your quote today.